Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| (Mark One) | |

| | REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR 12(G) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended March 31, 2023 |

| OR | |

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report……………

For the transition period from to

Commission file number 001‑36614

Alibaba Group Holding Limited

| (Exact name of Registrant as specified in its charter)Cayman Islands |

| (Jurisdiction of incorporation or organization) |

| 26/F Tower One, Times Square 1 Matheson Street, Causeway Bay Hong Kong S.A.R.People’s Republic of China |

| (Address of principal executive offices)Toby Hong Xu, Chief Financial Officer Telephone: +852‑2215‑5100 Facsimile: +852‑2215‑5200 Alibaba Group Holding Limited 26/F Tower One, Times Square 1 Matheson Street, Causeway Bay Hong Kong S.A.R.People’s Republic of China |

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Ordinary Shares, par value US$0.000003125 per share | 9988 (HKD Counter)89988 (RMB Counter) | The Stock Exchange of Hong Kong Limited |

| American Depositary Shares, each representing eight Ordinary Shares | BABA | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 20,526,017,712 Ordinary Shares

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S‑T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non‑accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

| Large accelerated filer | Accelerated filer | Non‑accelerated filer | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP | International Financial Reporting Standards as issued by the International Accounting Standards Board | Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Securities Exchange Act of 1934).

Yes No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes No

Table of Contents

TABLE OF CONTENTS

| Page | ||

| LETTER FROM OUR CHAIRMAN AND CEO TO SHAREHOLDERS | ii | |

| CONVENTIONS THAT APPLY TO THIS ANNUAL REPORT ON FORM 20‑F | iv | |

| FORWARD-LOOKING STATEMENTS | x | |

| PART I | ||

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 1 |

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE | 1 |

| ITEM 3. | KEY INFORMATION | 1 |

| ITEM 4. | INFORMATION ON THE COMPANY | 69 |

| ITEM 4A. | UNRESOLVED STAFF COMMENTS | 118 |

| ITEM 5. | OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 118 |

| ITEM 6. | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 150 |

| ITEM 7. | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 168 |

| ITEM 8. | FINANCIAL INFORMATION | 182 |

| ITEM 9. | THE OFFER AND LISTING | 183 |

| ITEM 10. | ADDITIONAL INFORMATION | 184 |

| ITEM 11. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 192 |

| ITEM 12. | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 193 |

| PART II | ||

| ITEM 13. | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 198 |

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 198 |

| ITEM 15. | CONTROLS AND PROCEDURES | 198 |

| ITEM 16A. | AUDIT COMMITTEE FINANCIAL EXPERT | 198 |

| ITEM 16B. | CODE OF ETHICS | 198 |

| ITEM 16C. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 199 |

| ITEM 16D. | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 199 |

| ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 199 |

| ITEM 16F. | CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT | 200 |

| ITEM 16G. | CORPORATE GOVERNANCE | 200 |

| ITEM 16H. | MINE SAFETY DISCLOSURE | 202 |

| ITEM 16I. | DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | 202 |

| ITEM 16J. | INSIDER TRADING POLICIES | 203 |

| PART III | ||

| ITEM 17. | FINANCIAL STATEMENTS | 203 |

| ITEM 18. | FINANCIAL STATEMENTS | 203 |

| ITEM 19. | EXHIBITS | 204 |

i

Table of Contents

LETTER FROM OUR CHAIRMAN AND CEO TO SHAREHOLDERS

Dear Shareholders,

Thank you for your continued trust, support, and recognition. Over the past year, we have collectively witnessed and experienced many significant events – we finally moved on from the pandemic, work and life got back on track, and the world reopened. New disruptive AI technology is changing how we view the world and understand reality, and there are high hopes for it to drive fundamental change across all aspects of the human experience.

During this time of big transformations, I appreciate the opportunity to share with you the series of important changes at Alibaba over the past year, along with our thoughts and outlook for the future.

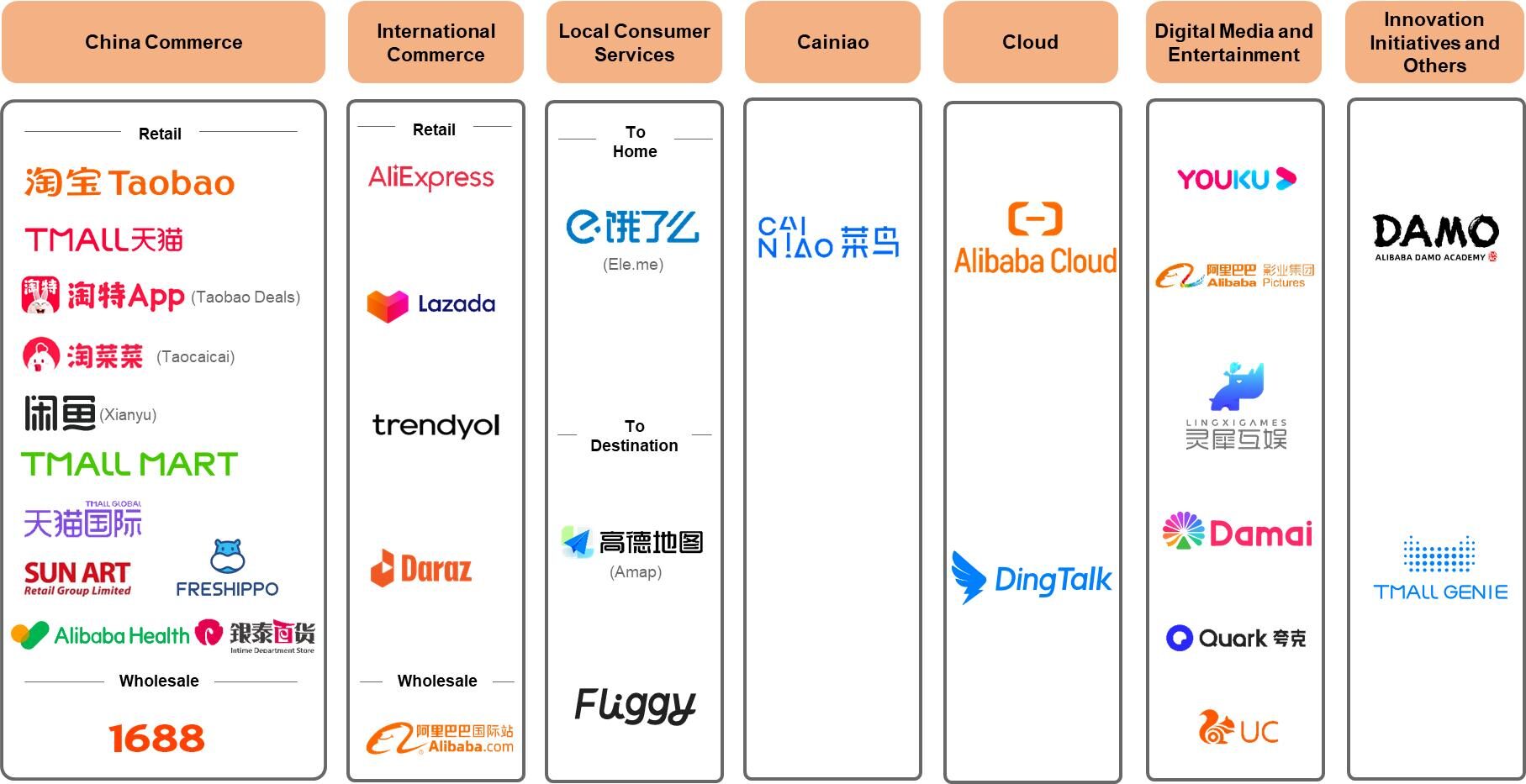

2023 is destined to be a year filled with significance in Alibaba history. Just before the end of the fiscal year, we announced a decision with far-reaching impact – after 24 years, Alibaba is evolving from a single company into a new governance model of “1+6+N” in which major business groups and various companies have independent operations. “1” represents Alibaba Group’s holding company, “6” refers to six major business groups – Cloud Intelligence Group, Taobao and Tmall Group, Local Services Group, Alibaba International Digital Commerce (AIDC) Group, Cainiao Smart Logistics Network Limited, and Digital Media and Entertainment Group, and “N” refers to various businesses such as Alibaba Health, Sun Art Retail, and Freshippo. Each entity in the “6+N” will establish its own board of directors that will provide oversight and support to the chief executive officer of the business. Moving forward, Alibaba Group will focus on implementing good capital management, supporting the healthy development of our major business groups and various companies, and fostering the development of new innovative businesses.

Over the last 24 years, the Alibaba family became quite diverse, with increasingly more creative and dynamic units. Our consumer-focused businesses in China served over one billion Chinese consumers last year. Cloud Intelligence Group is currently the world’s third largest and Asia Pacific’s largest cloud computing service provider. As of March 31, 2023, Cloud Intelligence Group has 86 availability zones across 28 regions worldwide, serving more than four million global customers, including 80% of China’s science and technology innovation enterprises, 60% of China’s national-level specialized “little giant” enterprises, and 55% of listed companies on the Chinese stock exchanges. AIDC Group served hundreds of millions of overseas consumers with a comprehensive selection of local and global products and holistic consumption experience, and reached over 47 million active SME buyers worldwide. Cainiao celebrated its tenth anniversary earlier this year, and is developing a world-class smart logistics network within China and across international markets. It processed over four million cross-border and international parcels daily in fiscal year 2023 and is working to offer a five-day delivery service for cross-border parcels in the future, starting from its main markets. The Local Services Group’s platform businesses have provided convenient “to-home” and “to-destination” services to hundreds of millions of Chinese consumers. On October 1, 2022, the digital map navigation platform Amap registered a peak record of 220 million daily active users. The Digital Media and Entertainment Group has focused on delivering “ordinary people, powerful feelings, positive energy” content, and several releases have generated wide influence. Under the new governance structure, these business groups will independently cater to their respective markets, become self-reliant, and find unique paths to greater growth. Except for Taobao and Tmall Group, all business groups and companies can raise external capital and potentially seek their own independent public offerings, subject to meeting the necessary conditions. To date, we have announced plans for the following transactions:

•

Cloud Intelligence Group will pursue a full spin-off from Alibaba Group via a stock dividend distribution to our shareholders and become an independent publicly listed company.

•

Cainiao Smart Logistics Network and Freshippo will seek independent public offerings, respectively.

•

AIDC Group will seek external capital.

Our organizational transformation is an unprecedented journey in the history of business in China and a daring experiment for a large-scale organization. As early as 2015, we introduced the “middle platform” strategy, then built the “large middle platform, small front office” organizational model, which supported our front line teams and became the industry benchmark. In 2020, we championed the development of an agile organization and gradually introduced greater management independence across our businesses. Internally we established a number of independently operated companies, including Cainiao Smart Logistics Network, Freshippo, and Local Services. In this latest development, we have progressed to the next stage of our transformation, which is the latest organizational governance structure of “1+6+N”.

Our robust balance sheet was instrumental in such a monumental transformation. Despite the challenges created by the global macroeconomic landscape, market fluctuations, and the pandemic, our businesses delivered solid progress. We generated approximately US$25 billion in free cash flow during the fiscal year. We used our abundant cash reserves to invest in new technologies, businesses, and great talent while continuing to execute our share repurchase program. During the fiscal year, we

ii

Table of Contents

repurchased approximately 130 million ADSs (the equivalent of one billion ordinary shares) for approximately US$10.9 billion and continued to explore different ways to create value for our shareholders.

At the beginning of 2023, I proposed “progress” as the keyword to set the tone for Alibaba’s development plans. “Progress” was necessary not only for the macro-environment changes and cyclical trends but also for Alibaba’s development trajectory. We believe the market is the best litmus test, and time will prove its worth. As we face a new era of unknowns, we hope to unleash our internal dynamism and creative forces through radical self-transformation that can withstand the test of the market and be positioned to capture the generational opportunities ahead. We believe our new governance structure will benefit the discovery and creation of value for our customers, business, and shareholders, and, hopefully, a chance to contribute greater value to the broader society.

Of course, some things will not change. Alibaba is unwavering in its commitment to focusing on the long-term, value creation, and the three strategies of consumption, cloud computing, and globalization. Over the last 20 years, we captured two historical opportunities: e-commerce in China’s consumer-focused Internet and cloud computing in China’s industrial Internet. Looking ahead, we will continue to serve hundreds of millions of households and support hundreds of thousands of industries through our two engines catering to the consumer Internet and industrial Internet, respectively. As the digital era begins its transition to the intelligent era, we must capture the generational opportunities associated with technology driving business transformation and the rapid changes in AI to create a larger runway for our businesses. We believe that AI’s contributions are not limited to efficiency improvements. We think it will create brand-new value.

As we begin this new chapter, Alibaba Group will welcome a new management team on September 10th. Joe will succeed me as the chairman of Alibaba Group, and Eddie as the chief executive officer of Alibaba Group. As for myself, I will be fully dedicated to my role as chairman and chief executive officer of our Cloud Intelligence Group and take on the new challenge of exploring the immense future in transforming and innovating with hundreds of thousands of industries through cloud computing, big data and AI.

The future is born out of our creations. Thank you again for your trust and support for Alibaba. I hope I will have the privilege of your companionship on the new journey, and may our future be extraordinary and full of miracles.

Daniel Zhang

Alibaba Group Chairman and Chief Executive Officer

Cloud Intelligence Group Chairman and Chief Executive Officer

July 2023

iii

Table of Contents

CONVENTIONS THAT APPLY TO THIS ANNUAL REPORT ON FORM 20‑F

Unless the context otherwise requires, references in this annual report on Form 20‑F to:

•

“2019 PRC Foreign Investment Law” are to the PRC Foreign Investment Law, promulgated by the National People’s Congress on March 15, 2019, which became effective on January 1, 2020;

•

“ADSs” are to the American depositary shares, each of which represents eight Shares;

•

“AI” are to artificial intelligence;

•

“Alibaba,” “Alibaba Group,” “company,” “our company,” “we,” “our” or “us” are to Alibaba Group Holding Limited, a company incorporated in the Cayman Islands with limited liability on June 28, 1999 and, where the context requires, its consolidated subsidiaries and its affiliated consolidated entities, including its variable interest entities and their subsidiaries, from time to time;

•

“Alibaba Health” are to Alibaba Health Information Technology Limited, a company incorporated in Bermuda on March 11, 1998, the shares of which are listed on the Main Board of the Hong Kong Stock Exchange (Stock Code: 0241), and, except where the context otherwise requires, its consolidated subsidiaries;

•

“Alibaba Pictures” are to Alibaba Pictures Group Limited, a company incorporated in Bermuda with limited liability on January 6, 1994, the shares of which are listed on the Main Board of the Hong Kong Stock Exchange (Stock Code: 1060) and, except where the context otherwise requires, its consolidated subsidiaries;

•

“Alipay” are to Alipay.com Co., Ltd., a company incorporated under the laws of the PRC on December 8, 2004, with which we have a long-term contractual relationship and which is a wholly-owned subsidiary of Ant Group or, where the context requires, its predecessor entities;

•

“Altaba” are to Altaba Inc. (formerly known as Yahoo! Inc.) and where the context requires, its consolidated subsidiaries; Altaba filed a certificate of dissolution with the Secretary of State of the State of Delaware, which became effective on October 4, 2019;

•

“Analysys” are to Analysys, a research institution;

•

“annual active consumers” are to user accounts that placed one or more confirmed orders through the relevant platform during the previous twelve months, regardless of whether or not the buyer and seller settle the transaction;

•

“Ant Group” are to Ant Group Co., Ltd. (formerly known as Ant Small and Micro Financial Services Group Co., Ltd.), a company organized under the laws of the PRC on October 19, 2000 and, as context requires, its consolidated subsidiaries;

•

“Articles” or “Articles of Association” are to our Articles of Association (as amended and restated from time to time), adopted on September 2, 2014;

•

“board” or “board of directors” are to our board of directors, unless otherwise stated;

•

“business day” are to any day (other than a Saturday, Sunday or public holiday) on which banks in relevant jurisdictions are generally open for business;

•

“Cainiao Network” are to Cainiao Smart Logistics Network Limited, a company incorporated on May 20, 2015 under the laws of the Cayman Islands and our consolidated subsidiary, together with its subsidiaries;

•

“CCASS” are to the Central Clearing and Settlement System established and operated by Hong Kong Securities Clearing Company Limited, a wholly-owned subsidiary of Hong Kong Exchange and Clearing Limited;

•

“China” and the “PRC” are to the People’s Republic of China;

iv

Table of Contents

•

“Companies (WUMP) Ordinance” are to the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32 of the Laws of Hong Kong), as amended or supplemented from time to time;

•

“CSRC” are to the China Securities Regulatory Commission of the PRC;

•

“Deposit Agreement” are to the deposit agreement, dated as of September 24, 2014, as amended, among us, Citibank, N.A. and our ADS holders and beneficial owners from time to time;

•

“director(s)” are to member(s) of our board, unless otherwise stated;

•

“DTC” are to The Depository Trust Company, the central book-entry clearing and settlement system for equity securities in the United States and the clearance system for our ADSs;

•

“Ele.me” are to Rajax Holding, a company incorporated under the laws of the Cayman Islands on June 8, 2011 and our consolidated subsidiary, and, except where the context otherwise requires, its consolidated subsidiaries and its affiliated consolidated entities, including its variable interest entities and their subsidiaries; where the context requires, also refers to our on-demand delivery and local services platform under the Ele.me brand;

•

“Enhanced VIE Structure” are to our enhanced structure for variable interest entities as described in “Item 4. Information on the Company — C. Organizational Structure”;

•

“EU” are to the European Union;

•

“FMCG” are to fast-moving consumer goods;

•

“foreign private issuer” are to such term as defined in Rule 3b-4 under the U.S. Exchange Act;

•

“Gartner” are to Gartner, Inc.; the Gartner content described herein (the “Gartner Content”) represent(s) research opinion or viewpoints published, as part of a syndicated subscription service, by Gartner, Inc. (“Gartner”), and are not representations of fact; Gartner Content speaks as of its original publication date (and not as of the date of this annual report), and the opinions expressed in the Gartner Content are subject to change without notice. GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally and is used herein with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose;

•

“GDP” are to gross domestic product;

•

“GDPR” are to the EU General Data Protection Regulation;

•

“GMV” are to the value of confirmed orders of products and services on our marketplaces, regardless of how, or whether, the buyer and seller settle the transaction; our calculation of GMV includes shipping charges paid by buyers to sellers; as a prudential matter aimed at eliminating any influence on our GMV of potentially fraudulent transactions, we exclude from our calculation of GMV transactions in certain product categories over certain amounts and transactions by buyers in certain product categories over a certain amount per day;

•

“HK$” or “Hong Kong dollars” or “HKD” are to Hong Kong dollars, the lawful currency of Hong Kong;

•

“Hong Kong” or “Hong Kong S.A.R.” are to the Hong Kong Special Administrative Region of the PRC;

•

“Hong Kong Listing Rules” are to the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited, as amended or supplemented from time to time;

•

“Hong Kong Share Registrar” are to Computershare Hong Kong Investor Services Limited;

v

Table of Contents

•

“Hong Kong Stock Exchange” are to The Stock Exchange of Hong Kong Limited;

•

“IaaS” are to infrastructure-as-a-service;

•

“ICP(s)” are to Internet content provider(s);

•

“IDC” are to International Data Corporation, a research institution;

•

“IoT” are to Internet of things;

•

“IPO” are to initial public offering;

•

“IT” are to information technology;

•

“Junao” are to Hangzhou Junao Equity Investment Partnership (Limited Partnership), a limited liability partnership incorporated under the laws of the PRC;

•

“Junhan” are to Hangzhou Junhan Equity Investment Partnership (Limited Partnership), a limited liability partnership incorporated under the laws of the PRC;

•

“Lazada” are to Lazada South East Asia Pte. Ltd., a company incorporated under the laws of the Republic of Singapore on January 19, 2012 and our consolidated subsidiary, and, except where the context otherwise requires, its consolidated subsidiaries and affiliated consolidated entities;

•

“major subsidiaries” are to the subsidiaries identified in our corporate structure chart in “Item 4. Information on the Company — C. Organizational Structure”;

•

“major variable interest entities” or “major VIEs” are to the variable interest entities that account for a significant majority of total revenue and assets of the variable interest entities as a group as described in “Item 3. Key Information — The VIE Structure Adopted by Our Company — Variable Interest Entity Financial Information”;

•

“Memorandum” are to our memorandum of association (as amended from time to time);

•

“MIIT” are to the Ministry of Industry and Information Technology of the PRC;

•

“MOF” are to the Ministry of Finance of the PRC;

•

“MOFCOM” are to the Ministry of Commerce of the PRC;

•

“MtCO2e” are to metric tons of carbon dioxide equivalent;

•

“NDRC” are to the National Development and Reform Commission of the PRC;

•

“NYSE” are to the New York Stock Exchange;

•

“orders” unless the context otherwise requires, are to each confirmed order from a transaction between a buyer and a seller for products and services on the relevant platform, even if the order includes multiple items, during the specified period, whether or not the transaction is settled;

•

our “wholesale marketplaces” are to 1688.com and Alibaba.com, collectively;

•

“P4P” are to pay-for-performance;

•

“PaaS” are to platform-as-a-service;

•

“PBOC” are to the People’s Bank of China;

vi

Table of Contents

•

“PCAOB” are to the Public Company Accounting Oversight Board;

•

“PRC government” or “State” are to the central government of the PRC, including all political subdivisions (including provincial, municipal and other regional or local government entities) and its organs or, as the context requires, any of them;

•

“Principal Share Registrar” are to Maples Fund Services (Cayman) Limited;

•

“QuestMobile” are to QuestMobile, a research institution;

•

“representative variable interest entities” or “representative VIEs” are to the variable interest entities identified in our corporate structure chart in “Item 4. Information on the Company — C. Organizational Structure”;

•

“RMB” or “Renminbi” are to Renminbi, the lawful currency of the PRC;

•

“RSU(s)” are to restricted share unit(s);

•

“SaaS” are to software-as-a-service;

•

“SAFE” are to the State Administration of Foreign Exchange of the PRC, the PRC governmental agency responsible for matters relating to foreign exchange administration, including local branches, when applicable;

•

“SAIC” are to State Administration for Industry and Commerce of the PRC, which has been merged into SAMR;

•

“SAMR” are to the State Administration for Market Regulation of the PRC;

•

“SAPA” are to a share and asset purchase agreement by and among us, Ant Group, Altaba, SoftBank and the other parties named therein, dated August 12, 2014, together with any subsequent amendments as the context requires;

•

“SEC” are to the United States Securities and Exchange Commission;

•

“SFC” are to the Securities and Futures Commission of Hong Kong;

•

“SFO” are to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong), as amended or supplemented from time to time;

•

“Share Split” are to the subdivision of each ordinary share into eight Shares, pursuant to which the par value of our Shares was correspondingly changed from US$0.000025 per Share to US$0.000003125 per Share, with effect from July 30, 2019; immediately after the Share Split became effective, our authorized share capital became US$100,000 divided into 32,000,000,000 Shares of par value US$0.000003125 per Share;

•

“shareholder(s)” are to holder(s) of Shares and, where the context requires, ADSs;

•

“Share(s)” or “ordinary share(s)” are to ordinary share(s) in our capital with par value of US$0.000003125 each;

•

“SMEs” are to small and medium‑sized enterprises;

•

“SoftBank” are to SoftBank Group Corp. (formerly known as SoftBank Corp.), and, except where the context otherwise requires, its consolidated subsidiaries;

•

“STA” are to the State Taxation Administration of the PRC;

•

“Sun Art” are to Sun Art Retail Group Limited, a company incorporated under the laws of Hong Kong on December 13, 2000 with limited liability, the shares of which are listed on the Main Board of the Hong Kong Stock Exchange (Stock Code: 6808), and except where the context requires, its consolidated subsidiaries;

•

“Takeovers Codes” are to Hong Kong’s Codes on Takeovers and Mergers and Share Buy-backs issued by the SFC;

vii

Table of Contents

•

“UK” are to the United Kingdom of Great Britain and Northern Ireland;

•

“U.S.” or “United States” are to the United States of America, its territories, its possessions and all areas subject to its jurisdiction;

•

“US$” or “U.S. dollars” are to the lawful currency of the United States;

•

“U.S. Exchange Act” are to the United States Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder;

•

“U.S. GAAP” are to accounting principles generally accepted in the United States;

•

“U.S. Securities Act” are to the United States Securities Act of 1933, as amended, and the rules and regulations promulgated thereunder;

•

“USTR” are to the Office of the U.S. Trade Representative;

•

“variable interest entities” or “VIE(s)” are to the variable interest entities that are incorporated and owned by PRC citizens or by PRC entities owned and/or controlled by PRC citizens, where applicable, that hold the ICP licenses, or other business operation licenses or approvals, and generally operate the various websites and/or mobile apps for our Internet businesses or other businesses in which foreign investment is restricted or prohibited, and are consolidated into our consolidated financial statements in accordance with U.S. GAAP;

•

“VAT” are to value-added tax; all amounts are exclusive of VAT in this annual report except where indicated otherwise;

•

“VIE structure” or “Contractual Arrangements” are to the variable interest entity structure;

•

“Youku” are to Youku Tudou Inc., a company incorporated under the laws of the Cayman Islands on September 20, 2005 and our indirect wholly-owned subsidiary, and, except where the context otherwise requires, its consolidated subsidiaries and its affiliated consolidated entities, including its variable interest entities and their subsidiaries; where the context requires, Youku also refers to our online video platform under the Youku brand; and

•

“Yunfeng Fund(s)” are to one or more Yunfeng investment funds established by Yunfeng Capital Limited or its affiliates, in which Jack Ma currently holds minority interest in the general partners.

viii

Table of Contents

Exchange Rate Information

Our reporting currency is the Renminbi. This annual report contains translations of Renminbi and Hong Kong dollar amounts into U.S. dollars at specific rates solely for the convenience of the reader. Unless otherwise stated, all translations of Renminbi and Hong Kong dollars into U.S. dollars and from U.S. dollars into Renminbi in this annual report were made at a rate of RMB6.8676 to US$1.00 and HK$7.8499 to US$1.00, the respective exchange rates on March 31, 2023 set forth in the H.10 statistical release of the Federal Reserve Board. We make no representation that any Renminbi, Hong Kong dollar or U.S. dollar amounts referred to in this annual report could have been, or could be, converted into U.S. dollars, Renminbi or Hong Kong dollars, as the case may be, at any particular rate or at all. On July 12, 2023, the noon buying rate for Renminbi and Hong Kong dollars was RMB7.1656 to US$1.00 and HK$7.8268 to US$1.00, respectively.

ix

Table of Contents

FORWARD-LOOKING STATEMENTS

This annual report on Form 20‑F contains forward‑looking statements. These statements are made under the “safe harbor” provision under Section 21E of the U.S. Exchange Act, and as defined in the Private Securities Litigation Reform Act of 1995. Forward‑looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “future,” “aim,” “estimate,” “intend,” “seek,” “plan,” “believe,” “potential,” “continue,” “ongoing,” “target,” “guidance,” “is/are likely to” or other similar expressions. The forward‑looking statements included in this annual report relate to, among others:

•

our new organizational and governance structure, strategic benefits of this new structure and future spin-off or capital raising plans;

•

our growth strategies and business plans;

•

our future business development, results of operations and financial condition;

•

trends and competition in commerce, cloud computing and digital media and entertainment industries and the other industries in which we operate, both in China and globally, as well as trends in overall technology;

•

our continuing investments in our businesses;

•

expected changes in our revenues and certain cost and expense items and our margins;

•

fluctuations in general economic and business conditions in China and globally;

•

international trade policies, protectionist policies and other policies (including those relating to export control and economic or trade sanctions) that could place restrictions on economic and commercial activity;

•

the regulatory environment in which we and companies integral to our ecosystem operate in China and globally;

•

expected results of regulatory investigations, litigations and other proceedings;

•

impacts of the COVID-19 pandemic;

•

our sustainability goals; and

•

assumptions underlying or related to any of the foregoing.

Forward-looking statements involve inherent risks and uncertainties. A number of factors could cause actual results to differ materially from those contained in any forward-looking statement. These factors include but are not limited to the following: our corporate structure, including the VIE structure we use to operate certain businesses in the PRC; the implementation of our new organizational and governance structure and the execution of spin-off or capital raising plans of our subsidiaries; our ability to maintain the trusted status of our ecosystem; our ability to compete, innovate and maintain or grow our revenue or business, including expanding our international and cross-border businesses and operations and managing a large and complex organization; risks associated with sustained investments in our businesses; fluctuations in general economic and business conditions in China and globally; uncertainties arising from competition among countries and geopolitical tensions, including protectionist or national security policies and export control, economic or trade sanctions; risks associated with our acquisitions, investments and alliances; uncertainties and risks associated with a broad range of complex laws and regulations (including in the areas of data security and privacy protection, anti-monopoly and anti-unfair competition, content regulation, consumer protection and regulation of Internet platforms) in the PRC and globally; cybersecurity risks; impacts of the COVID-19 pandemic and assumptions underlying or related to any of the foregoing. Please also see “Item 3. Key Information — D. Risk Factors.”

The forward‑looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report and are based on current expectations, assumptions, estimates and projections. We undertake no obligation to update any forward‑looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we have referred to in this annual report completely and with the understanding that our actual future results may be materially different from what we expect.

x

Table of Contents

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

The VIE Structure Adopted by Our Company

Risks Related to the VIE Structure

Alibaba Group Holding Limited is a Cayman Islands holding company. It does not directly engage in business operations itself. Due to PRC legal restrictions on foreign ownership and investment in certain industries, we, similar to all other entities with foreign-incorporated holding company structures operating in our industry in China, operate our Internet businesses and other businesses in which foreign investment is restricted or prohibited in the PRC through variable interest entities, or VIEs. The VIEs are incorporated and owned by PRC citizens or by PRC entities owned and/or controlled by PRC citizens, and not by our company. We and, through us, our shareholders do not own any equity interests in the VIEs. Investors in our ADSs and Shares are purchasing equity securities of a Cayman Islands holding company rather than equity securities issued by our consolidated subsidiaries and the VIEs, and investors may never hold equity interests in the VIEs under current PRC laws and regulations.

Investing in our company involves unique risks related to the VIE structure adopted by our company. In particular, if the PRC government deems that the contractual arrangements in relation to the VIEs do not comply with PRC regulations on foreign investment, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to penalties, or be forced to relinquish our interests in the operation of the VIEs, and we would no longer be able to consolidate the financial results of the VIEs in our consolidated financial statements. This would likely materially and adversely affect our business, financial results and the trading prices of our ADSs, Shares and/or other securities, including causing the trading prices of such securities to significantly decline or become worthless. Contractual arrangements in relation to VIEs have not been tested in a court of law. See “— D. Risk Factors — Risks Related to Our Corporate Structure” for more details on the risks relating to the VIE structure.

1

Table of Contents

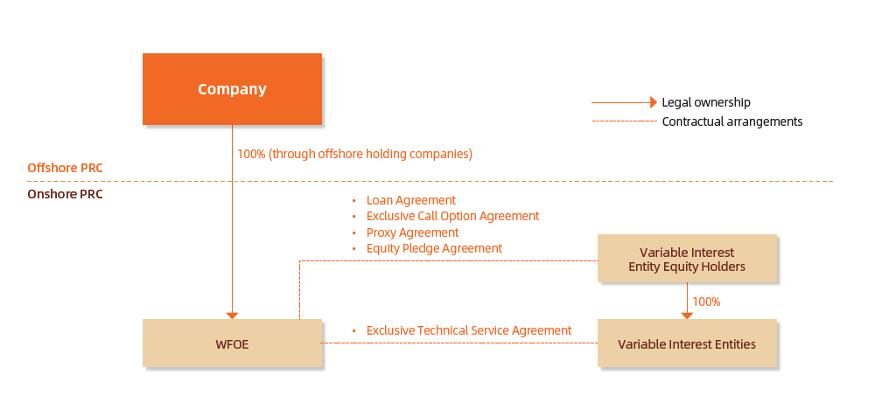

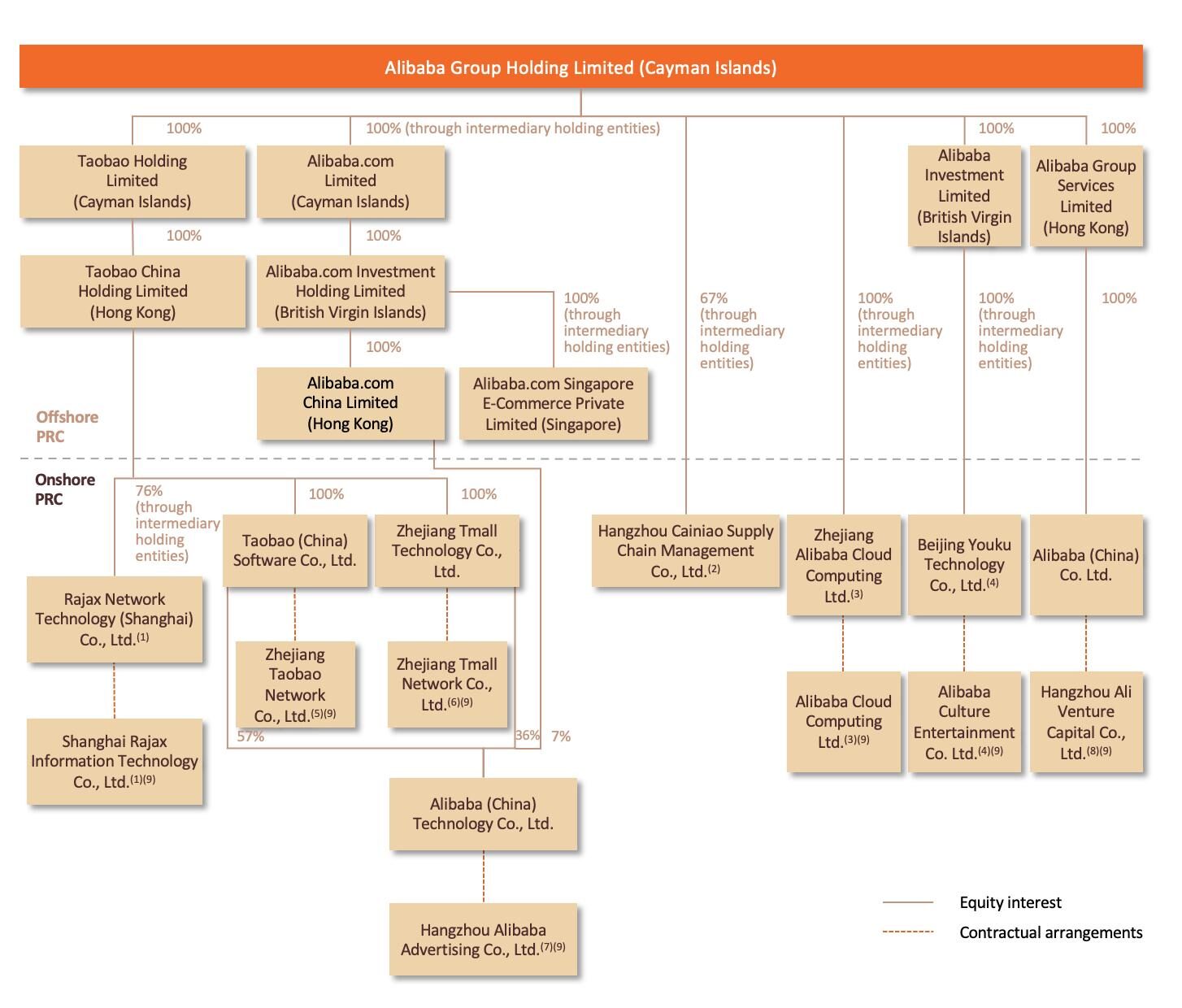

Our Corporate Structure

Like many large scale, multinational companies with businesses around the world and across industries, we conduct our business through a large number of Chinese and foreign operating entities, including VIEs. The chart below summarizes our corporate structure as of March 31, 2023 and identifies the subsidiaries and VIEs that together are representative of the major businesses operated by our group, including our significant subsidiaries, as that term is defined under Section 1-02 of Regulation S-X under the U.S. Securities Act, and other representative subsidiaries, which we collectively refer to as our major subsidiaries, as well the corresponding representative VIEs, which we refer to as the representative VIEs:

(1)

Primarily involved in the operation of local consumer services businesses.

(2)

Primarily involved in the operation of Cainiao business.

(3)

Primarily involved in the operation of cloud business.

(4)

Primarily involved in the operation of digital media and entertainment business.

(5)

Primarily involved in the operation of Taobao.

(6)

Primarily involved in the operation of Tmall.

(7)

Primarily involved in the operation of our wholesale marketplaces and cross-border commerce retail and wholesale businesses.

(8)

Primarily involved in investment projects.

(9)

A VIE.

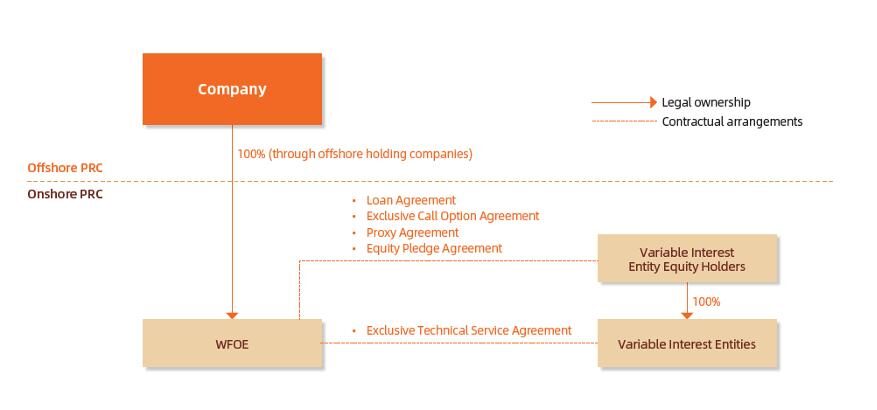

VIE Structure

The contractual relationships with the VIEs provide us the power to direct the activities of the VIEs and the obligation to absorb losses or the right to receive benefits from the VIEs, such that we are the primary beneficiary for accounting purposes

2

Table of Contents

and therefore consolidate the VIEs. As a result, we include the financial results of each of the VIEs in our consolidated financial statements in accordance with U.S. GAAP.

The following diagram is a simplified illustration of the typical ownership structure and contractual arrangements for VIEs:

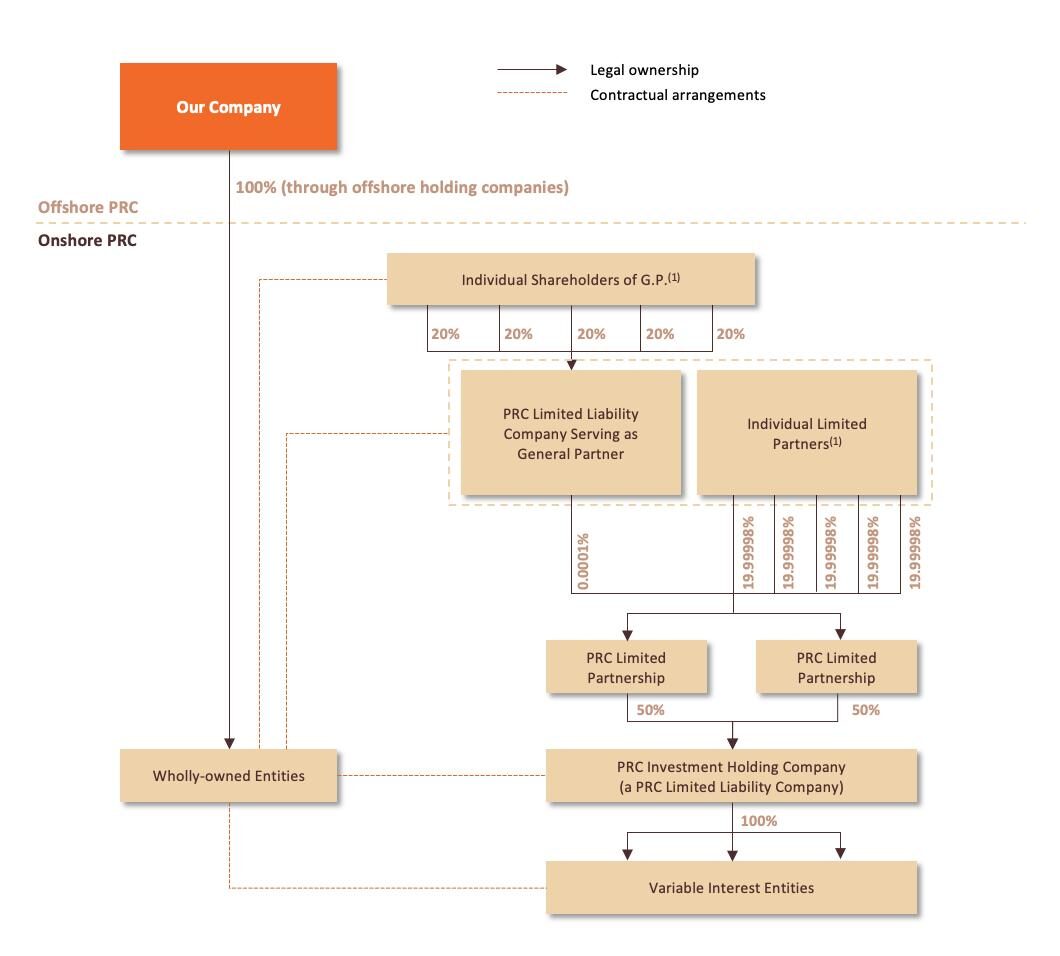

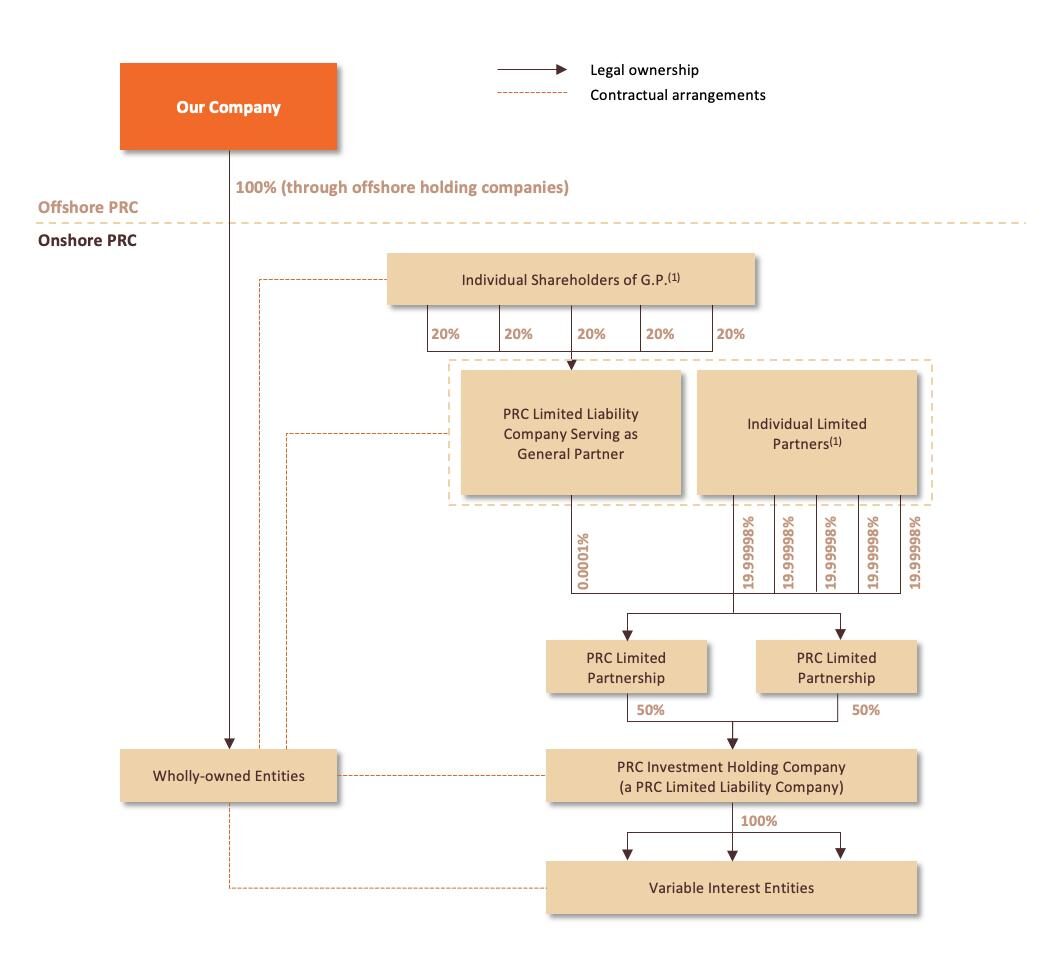

For most of the VIEs, our group uses a different structure, or the Enhanced VIE Structure. The Enhanced VIE Structure maintains the primary legal framework that we and many peer companies in our industry have adopted to operate businesses in which foreign investment is restricted or prohibited in the PRC. We may also create additional holding structures in the future.

Under the Enhanced VIE Structure, a VIE is typically held by a PRC limited liability company, instead of individuals. This PRC limited liability company is directly or indirectly owned by two PRC limited partnerships, each of which holds 50% of the equity interest. Each of these partnerships is comprised of (i) a PRC limited liability company, as general partner (which is formed by a number of selected members of the Alibaba Partnership and our management who are PRC citizens), and (ii) the same group of natural persons, as limited partners. Under the terms of the relevant partnership agreements, the natural person limited partners must be members of the Alibaba Partnership or our management who are PRC citizens and as designated by the general partner of the partnership.

For our representative VIEs, these individuals are Daniel Yong Zhang, Jessie Junfang Zheng, Xiaofeng Shao, Zeming Wu and Fang Jiang (with respect to each of Zhejiang Taobao Network Co., Ltd., Zhejiang Tmall Network Co., Ltd., Hangzhou Alibaba Advertising Co., Ltd., Hangzhou Ali Venture Capital Co., Ltd., Shanghai Rajax Information Technology Co., Ltd. and Alibaba Cloud Computing Ltd.), and Jeff Jianfeng Zhang, Winnie Jia Wen, Jie Song, Yongxin Fang and Li Cheng (with respect to Alibaba Culture Entertainment Co., Ltd.). Because Li Cheng is no longer a member of the Alibaba Partnership, we are in the process of replacing him. In addition, we are in the process of restructuring the VIEs and changing these individuals as part of our Reorganization.

Under the Enhanced VIE Structure, the designated subsidiary, on the one hand, and the corresponding VIE and the multiple layers of legal entities above the VIE, as well as the natural persons described above, on the other hand, enter into contractual arrangements, which are substantially similar to the contractual arrangements we have historically used for VIEs.

3

Table of Contents

The following diagram is a simplified illustration of the typical ownership structure and contractual arrangements of the VIEs under the Enhanced VIE Structure:

(1)

Selected members of the Alibaba Partnership or our management who are PRC citizens.

Loan Agreements

Pursuant to the relevant loan agreement, our respective subsidiary has granted a loan to the relevant VIE equity holders, which may only be used for the purpose of its business operation activities agreed by our subsidiary or the acquisition of the relevant VIE.

Exclusive Call Option Agreements

Under the Enhanced VIE Structure, each relevant VIE and its equity holders have jointly granted our relevant subsidiary (A) an exclusive call option to request the relevant VIE to decrease its registered capital and (B) an exclusive call option to subscribe for any increased capital of relevant VIE.

4

Table of Contents

Proxy Agreements

Pursuant to the relevant proxy agreement, each of the VIE equity holders irrevocably authorizes any person designated by our subsidiary to exercise the rights of the equity holder of the VIE, including without limitation the right to vote and appoint directors.

Equity Pledge Agreements

Pursuant to the relevant equity pledge agreement, the relevant VIE equity holders have pledged all of their interests in the equity of the VIE as a continuing first priority security interest in favor of the corresponding subsidiary to secure the outstanding amounts advanced under the relevant loan agreements described above and to secure the performance of obligations by the VIE and/or its equity holders under the other structure contracts. Each subsidiary is entitled to exercise its right to dispose of the VIE equity holders’ pledged interests in the equity of the VIE and has priority in receiving payment by the application of proceeds from the auction or sale of the pledged interests, in the event of any breach or default under the loan agreement or other structure contracts, if applicable.

Exclusive Services Agreements

Under the Enhanced VIE Structure, each relevant VIE has entered into an exclusive service agreement with the respective subsidiary, pursuant to which our relevant subsidiary provides exclusive services to the VIE. In exchange, the VIE pays a service fee to our subsidiary, the amount of which shall be determined, to the extent permitted by applicable PRC laws as proposed by our subsidiary, resulting in a transfer of substantially all of the profits from the VIE to our subsidiary.

For a more detailed summary of such contractual arrangements, see “Item 4. Information on the Company — C. Organizational Structure.”

If the VIEs or their equity holders fail to perform their respective obligations under the contractual arrangements, we will have to enforce our rights under the contractual arrangements through the operations of PRC law and arbitral or judicial agencies, which may be costly and time-consuming and will be subject to uncertainties in the PRC legal system, including the uncertainty resulting from the fact that these VIE contracts have not been tested in a PRC court. Consequently, the contractual arrangements may not be as effective in ensuring our control over the relevant portion of our business operations as direct ownership. The contractual arrangements are governed by PRC law and provide for the resolution of disputes through arbitration or court proceedings in China. Accordingly, these contracts would be interpreted in accordance with PRC law and any disputes would be resolved in accordance with PRC legal procedures. Uncertainties regarding the interpretation and enforcement of the relevant PRC laws and regulations could limit our ability to enforce the contractual arrangements. Under PRC law, if the losing parties fail to carry out the arbitration awards or court judgments within a prescribed time limit, the prevailing parties may only enforce the arbitration awards or court judgments in PRC courts, which would require additional expense and delay. In the event we are unable to enforce the contractual arrangements, we may not be able to exert effective control over the VIEs, and our ability to conduct our business, as well as our financial condition and results of operations, may be materially and adversely affected. See “— D. Risk Factors — Risks Related to Our Corporate Structure — Our contractual arrangements may not be as effective in providing control over the VIEs as direct ownership” and “— Any failure by the VIEs or their equity holders to perform their obligations under the contractual arrangements would have a material adverse effect on our business, financial condition and results of operations. ”

Variable Interest Entity Financial Information

The following tables present the condensed consolidating schedule of operations and cash flows information for the fiscal years ended March 31, 2021, 2022 and 2023, and condensed consolidating schedule of balance sheet information as of March 31,2022 and 2023 for:

•

Alibaba Group Holding Limited (“Parent”);

•

the variable interest entities, including their subsidiaries, that together account for a significant majority of total revenue and assets of the variable interest entities as a group, which we collectively refer to as the “major variable interest entities and their subsidiaries”;

•

subsidiaries that are, for accounting purposes only, the primary beneficiaries of the major variable interest entities; and

5

Table of Contents

•

other subsidiaries and consolidated entities, which include variable interest entities that are not major variable interest entities.

We conduct our business through a large number of subsidiaries and consolidated entities. We are presenting the condensed consolidating information for the major variable interest entities only. We believe this presentation provides a reasonably adequate basis for investors to evaluate the assets, operations and overall significance of the variable interest entities as a group, as well as the nature and amounts associated with intercompany transactions. The large number of variable interest entities not included as major variable interest entities are individually, and in the aggregate, not material for our company taken as a whole. To include them in the presentation would require tremendous time and efforts to prepare condensed consolidating schedules for them, which we do not believe would provide meaningful additional information to investors.

The amounts shown in the tables do not reconcile directly to financial information presented for the variable interest entities in our audited consolidated financial statements.

Although the variable interest entities hold licenses and approvals and assets for regulated activities that are necessary for our business operations, as well as certain equity investments in businesses, to which foreign investments are typically restricted or prohibited under applicable PRC law, we hold the significant majority of assets and operations in our subsidiaries and the significant majority of our revenue is captured directly by our subsidiaries. Therefore, our subsidiaries directly capture the significant majority of the profits and associated cash flow from operations, without having to rely on contractual arrangements to transfer cash flow from the variable interest entities to our subsidiaries.

| For the year ended March 31, 2023 | ||||||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | US$ | ||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||||||

| Revenue from third parties | — | 709,421 | 88,121 | 71,145 | — | 868,687 | 126,491 | |||||||||||||||||||||

| Revenue from group companies | — | 29,159 | 5,671 | 136,113 | (170,943 | ) | — | — | ||||||||||||||||||||

| Total cost and expenses | (846 | ) | (763,158 | ) | (97,402 | ) | (1) | (168,473 | ) | 261,543 | (768,336 | ) | (111,879 | ) | ||||||||||||||

| Income from subsidiaries and VIEs | 84,000 | 100,379 | — | 3,031 | (187,410 | ) | — | — | ||||||||||||||||||||

| Income (loss) from operations | 83,154 | 75,801 | (3,610 | ) | 41,816 | (96,810 | ) | 100,351 | 14,612 | |||||||||||||||||||

| Other income and expenses | (10,645 | ) | 11,003 | 6,557 | 72,519 | (90,600 | ) | (11,166 | ) | (1,626 | ) | |||||||||||||||||

| Income tax expenses | — | (6,551 | ) | 117 | (9,115 | ) | — | (15,549 | ) | (2,264 | ) | |||||||||||||||||

| Share of results of equity method investees | — | (3,176 | ) | (46 | ) | (4,841 | ) | — | (8,063 | ) | (1,174 | ) | ||||||||||||||||

| Net income | 72,509 | 77,077 | 3,018 | 100,379 | (187,410 | ) | 65,573 | 9,548 | ||||||||||||||||||||

| Net loss attributable to noncontrolling interests | — | 7,197 | 13 | — | — | 7,210 | 1,050 | |||||||||||||||||||||

| Accretion of mezzanine equity | — | (274 | ) | — | — | — | (274 | ) | (40 | ) | ||||||||||||||||||

| Net income attributable to ordinary shareholders | 72,509 | 84,000 | 3,031 | 100,379 | (187,410 | ) | 72,509 | 10,558 | ||||||||||||||||||||

| For the year ended March 31, 2022 | ||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Revenue from third parties | — | 691,997 | 87,337 | 73,728 | — | 853,062 | ||||||||||||||||||

| Revenue from group companies | — | 75,610 | 8,485 | 160,947 | (245,042 | ) | — | |||||||||||||||||

| Total cost and expenses | (444 | ) | (771,883 | ) | (96,262 | ) | (1) | (189,014 | ) | 274,179 | (783,424 | ) | ||||||||||||

| Income from subsidiaries and VIEs | 63,745 | 81,515 | — | 5,284 | (150,544 | ) | — | |||||||||||||||||

| Income (loss) from operations | 63,301 | 77,239 | (440 | ) | 50,945 | (121,407 | ) | 69,638 | ||||||||||||||||

| Other income and expenses | (1,342 | ) | (27,923 | ) | 5,227 | 43,087 | (29,137 | ) | (10,088 | ) | ||||||||||||||

| Income tax expenses | — | (15,506 | ) | (258 | ) | (11,051 | ) | — | (26,815 | ) | ||||||||||||||

| Share of results of equity method investees | — | 15,055 | 755 | (1,466 | ) | — | 14,344 | |||||||||||||||||

| Net income | 61,959 | 48,865 | 5,284 | 81,515 | (150,544 | ) | 47,079 | |||||||||||||||||

| Net loss attributable to noncontrolling interests | — | 15,170 | — | — | — | 15,170 | ||||||||||||||||||

| Accretion of mezzanine equity | — | (290 | ) | — | — | — | (290 | ) | ||||||||||||||||

| Net income attributable to ordinary shareholders | 61,959 | 63,745 | 5,284 | 81,515 | (150,544 | ) | 61,959 | |||||||||||||||||

6

Table of Contents

| For the year ended March 31, 2021 | ||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Revenue from third parties | — | 563,077 | 71,455 | 82,757 | — | 717,289 | ||||||||||||||||||

| Revenue from group companies | — | 85,667 | 10,854 | 165,263 | (261,784 | ) | — | |||||||||||||||||

| Total cost and expenses | (614 | ) | (658,139 | ) | (83,164 | ) | (1) | (178,855 | ) | 293,161 | (627,611 | ) | ||||||||||||

| Income from subsidiaries and VIEs | 150,515 | 107,740 | — | 3,362 | (261,617 | ) | — | |||||||||||||||||

| Income (loss) from operations | 149,901 | 98,345 | (855 | ) | 72,527 | (230,240 | ) | 89,678 | ||||||||||||||||

| Other income and expenses | 407 | 47,377 | 5,940 | 53,553 | (31,377 | ) | 75,900 | |||||||||||||||||

| Income tax expenses | — | (16,959 | ) | (1,249 | ) | (11,070 | ) | — | (29,278 | ) | ||||||||||||||

| Share of results of equity method investees | — | 14,825 | (571 | ) | (7,270 | ) | — | 6,984 | ||||||||||||||||

| Net income | 150,308 | 143,588 | 3,265 | 107,740 | (261,617 | ) | 143,284 | |||||||||||||||||

| Net loss attributable to noncontrolling interests | — | 7,197 | 97 | — | — | 7,294 | ||||||||||||||||||

| Accretion of mezzanine equity | — | (270 | ) | — | — | — | (270 | ) | ||||||||||||||||

| Net income attributable to ordinary shareholders | 150,308 | 150,515 | 3,362 | 107,740 | (261,617 | ) | 150,308 | |||||||||||||||||

Note:

(1)

These include technical service fee incurred by major VIEs and their subsidiaries for exclusive technical service provided by primary beneficiaries of major VIEs to major VIEs and their subsidiaries in the amounts of RMB18,698 million, RMB17,225 million and RMB15,445 million (US$2,249 million) for the years ended March 31, 2021, 2022 and 2023, respectively.

| For the year ended March 31, 2023 | ||||||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | US$ | ||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||||||

| Net cash provided by operating activities | 71,885 | (1) | 154,186 | 3,622 | 196,309 | (226,250 | ) | 199,752 | 29,086 | |||||||||||||||||||

| Net cash used in investing activities | (12,290 | ) | (1) | (87,248 | ) | (2,003 | ) | (2) | (100,132 | ) | 66,167 | (135,506 | ) | (19,731 | ) | |||||||||||||

| Net cash (used in) provided by financing activities | (59,439 | ) | (1) | (83,590 | ) | 1,766 | (2) | (84,439 | ) | 160,083 | (65,619 | ) | (9,555 | ) | ||||||||||||||

| Effect of exchange rate changes on cash and cash equivalents, restricted cash and escrow receivables | 33 | 3,495 | 2 | — | — | 3,530 | 514 | |||||||||||||||||||||

| Increase (Decrease) in cash and cash equivalents, restricted cash and escrow receivables | 189 | (13,157 | ) | 3,387 | 11,738 | — | 2,157 | 314 | ||||||||||||||||||||

| Cash and cash equivalents, restricted cash and escrow receivables at the beginning of the year | 387 | 175,866 | 4,537 | 46,563 | — | 227,353 | 33,105 | |||||||||||||||||||||

| Cash and cash equivalents, restricted cash and escrow receivables at the end of the year | 576 | 162,709 | 7,924 | 58,301 | — | 229,510 | 33,419 | |||||||||||||||||||||

Notes:

(1)

For the year ended March 31, 2023, the cash transfer from the parent to our subsidiaries amounting to RMB32,025 million (US$4,663 million), of which RMB31,088 million (US$4,527 million) and RMB937 million (US$136 million) were included in the parent’s net cash used in investing activities and financing activities, respectively.

For the year ended March 31, 2023, the cash transfer from our subsidiaries to the parent amounting to RMB112,153 million (US$16,331 million), of which RMB75,355 million (US$10,973 million), RMB20,565 million (US$2,994 million) and RMB16,233 million (US$2,364 million) were included in the parent’s net cash provided by operating activities, net cash used in investing activities and financing activities, respectively.

(2)

For the year ended March 31, 2023, the cash transfer from our subsidiaries and consolidated entities to the major VIEs and their subsidiaries amounting to RMB21,283 million (US$3,099 million), of which RMB11,858 million (US$1,727 million) and RMB9,425 million (US$1,372 million) were included in the major VIEs and their subsidiaries’ net cash used in investing activities and net cash provided by financing activities, respectively.

For the year ended March 31, 2023, the cash transfer from the major VIEs and their subsidiaries to our subsidiaries and consolidated entities amounting to RMB14,172 million (US$2,064 million), of which RMB6,513 million (US$949 million) and RMB7,659 million (US$1,115 million) were included in the major VIEs and their subsidiaries’ net cash used in investing activities and net cash provided by financing activities, respectively.

(3)

See “— Holding Company Structure and Cash Flows through Our Company” for nature of cash transfers mentioned above.

7

Table of Contents

| For the year ended March 31, 2022 | ||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Net cash (used in) provided by operating activities | (4,739 | ) | 219,750 | 18,811 | 21,498 | (112,561 | ) | 142,759 | ||||||||||||||||

| Net cash used in investing activities | (20,188 | ) | (1) | (235,528 | ) | (15,672 | ) | (2) | (32,365 | ) | 105,161 | (198,592 | ) | |||||||||||

| Net cash provided by (used in) financing activities | 24,920 | (1) | (51,502 | ) | (9,099 | ) | (2) | (36,168 | ) | 7,400 | (64,449 | ) | ||||||||||||

| Effect of exchange rate changes on cash and cash equivalents, restricted cash and escrow receivables | (36 | ) | (8,798 | ) | — | — | — | (8,834 | ) | |||||||||||||||

| Decrease in cash and cash equivalents, restricted cash and escrow receivables | (43 | ) | (76,078 | ) | (5,960 | ) | (47,035 | ) | — | (129,116 | ) | |||||||||||||

| Cash and cash equivalents, restricted cash and escrow receivables at the beginning of the year | 430 | 251,944 | 10,497 | 93,598 | — | 356,469 | ||||||||||||||||||

| Cash and cash equivalents, restricted cash and escrow receivables at the end of the year | 387 | 175,866 | 4,537 | 46,563 | — | 227,353 | ||||||||||||||||||

Notes:

(1)

For the year ended March 31, 2022, the cash transfer from the parent to our subsidiaries amounting to RMB20,188 million was included in the parent’s net cash used in investing activities.

For the year ended March 31, 2022, the cash transfer from our subsidiaries to the parent amounting to RMB95,621 million was included in the parent’s net cash provided by financing activities.

(2)

For the year ended March 31, 2022, the cash transfer from our subsidiaries and consolidated entities to the major VIEs and their subsidiaries amounting to RMB2,539 million, of which RMB35 million and RMB2,504 million were included in the major VIEs and their subsidiaries’ net cash used in investing activities and financing activities, respectively.

For the year ended March 31, 2022, the cash transfer from the major VIEs and their subsidiaries to our subsidiaries and consolidated entities amounting to RMB24,404 million, of which RMB11,774 million and RMB12,630 million were included in the major VIEs and their subsidiaries’ net cash used in investing activities and financing activities, respectively.

| For the year ended March 31, 2021 | ||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Net cash provided by operating activities | 33,796 | (1) | 210,082 | 808 | 56,727 | (69,627 | ) | 231,786 | ||||||||||||||||

| Net cash used in investing activities | (70,623 | ) | (1) | (147,242 | ) | (17,764 | ) | (2) | (70,138 | ) | 61,573 | (244,194 | ) | |||||||||||

| Net cash provided by (used in) financing activities | 36,570 | (1) | (31,875 | ) | 13,726 | (2) | 3,607 | 8,054 | 30,082 | |||||||||||||||

| Effect of exchange rate changes on cash and cash equivalents, restricted cash and escrow receivables | (114 | ) | (7,073 | ) | — | — | — | (7,187 | ) | |||||||||||||||

| (Decrease) Increase in cash and cash equivalents, restricted cash and escrow receivables | (371 | ) | 23,892 | (3,230 | ) | (9,804 | ) | — | 10,487 | |||||||||||||||

| Cash and cash equivalents, restricted cash and escrow receivables at the beginning of the year | 801 | 228,052 | 13,727 | 103,402 | — | 345,982 | ||||||||||||||||||

| Cash and cash equivalents, restricted cash and escrow receivables at the end of the year | 430 | 251,944 | 10,497 | 93,598 | — | 356,469 | ||||||||||||||||||

Notes:

(1)

For the year ended March 31, 2021, the cash transfer from the parent to our subsidiaries amounting to RMB70,623 million was included in the parent’s net cash used in investing activities.

For the year ended March 31, 2021, the cash transfer from our subsidiaries to the parent amounting to RMB43,078 million, of which RMB37,918 million and RMB5,160 million were included in the parent’s net cash provided by operating activities and financing activities, respectively.

(2)

For the year ended March 31, 2021, the cash transfer from our subsidiaries and consolidated entities to the major VIEs and their subsidiaries amounting to RMB20,865 million, of which RMB175 million and RMB20,690 million were included in the major VIEs and their subsidiaries’ net cash used in investing activities and net cash provided by financing activities, respectively.

For the year ended March 31, 2021, the cash transfer from the major VIEs and their subsidiaries to our subsidiaries and consolidated entities amounting to RMB5,575 million, of which RMB682 million and RMB4,893 million were included in the major VIEs and their subsidiaries’ net cash used in investing activities and net cash provided by financing activities, respectively.

8

Table of Contents

| As of March 31, 2023 | ||||||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | US$ | ||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||||||

| Cash and cash equivalents and short-term investments | 576 | 301,264 | 22,301 | 195,437 | — | 519,578 | 75,656 | |||||||||||||||||||||

| Investments in equity method investees and equity securities and other investments | — | 375,195 | 32,556 | 50,258 | — | 458,009 | 66,691 | |||||||||||||||||||||

| Accounts receivable, net of allowance | — | 14,165 | 17,084 | 885 | — | 32,134 | 4,679 | |||||||||||||||||||||

| Amounts due from group companies | 99,536 | 319,591 | 19,812 | 208,070 | (647,009 | ) | — | — | ||||||||||||||||||||

| Prepayments and other assets | 868 | 186,896 | 15,334 | 49,190 | — | 252,288 | 36,737 | |||||||||||||||||||||

| Interest in subsidiaries and VIEs | 1,123,451 | 217,954 | — | 5,850 | (1,347,255 | ) | — | — | ||||||||||||||||||||

| Property and equipment and intangible assets | — | 193,827 | 8,910 | 20,207 | — | 222,944 | 32,463 | |||||||||||||||||||||

| Goodwill | — | 266,133 | 1,958 | — | — | 268,091 | 39,037 | |||||||||||||||||||||

| Total assets | 1,224,431 | 1,875,025 | 117,955 | 529,897 | (1,994,264 | ) | 1,753,044 | 255,263 | ||||||||||||||||||||

| Amounts due to group companies | 103,507 | 243,398 | 66,683 | 233,421 | (647,009 | ) | — | — | ||||||||||||||||||||

| Accrued and other liabilities | 131,267 | 317,945 | 32,040 | 74,016 | — | 555,268 | 80,853 | |||||||||||||||||||||

| Deferred revenue and customer advances | — | 57,100 | 13,249 | 4,506 | — | 74,855 | 10,900 | |||||||||||||||||||||

| Total liabilities | 234,774 | 618,443 | 111,972 | 311,943 | (647,009 | ) | 630,123 | 91,753 | ||||||||||||||||||||

| Mezzanine equity | — | 9,858 | — | — | — | 9,858 | 1,435 | |||||||||||||||||||||

| Total shareholders’ equity | 989,657 | 1,123,451 | 5,850 | 217,954 | (1,347,255 | ) | 989,657 | 144,105 | ||||||||||||||||||||

| Noncontrolling interests | — | 123,273 | 133 | — | — | 123,406 | 17,970 | |||||||||||||||||||||

| Total liabilities, mezzanine equity and equity | 1,224,431 | 1,875,025 | 117,955 | 529,897 | (1,994,264 | ) | 1,753,044 | 255,263 | ||||||||||||||||||||

| As of March 31, 2022 | ||||||||||||||||||||||||

| Parent | Other Subsidiaries and Consolidated Entities | Major VIEs and their Subsidiaries | Primary Beneficiaries of Major VIEs | Eliminations | Consolidated Total | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | RMB | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Cash and cash equivalents and short-term investments | 387 | 272,254 | 14,208 | 159,563 | — | 446,412 | ||||||||||||||||||

| Investments in equity method investees and equity securities and other investments | — | 397,390 | 33,989 | 20,547 | — | 451,926 | ||||||||||||||||||

| Accounts receivable, net of allowance | — | 11,853 | 20,074 | 886 | — | 32,813 | ||||||||||||||||||

| Amounts due from group companies | 163,476 | 282,817 | 23,556 | 174,120 | (643,969 | ) | — | |||||||||||||||||

| Prepayments and other assets | 767 | 198,263 | 14,227 | 50,527 | — | 263,784 | ||||||||||||||||||

| Interest in subsidiaries and VIEs | 994,066 | 114,798 | — | (129 | ) | (1,108,735 | ) | — | ||||||||||||||||

| Property and equipment and intangible assets | — | 198,691 | 6,972 | 25,374 | — | 231,037 | ||||||||||||||||||

| Goodwill | — | 267,548 | 2,033 | — | — | 269,581 | ||||||||||||||||||

| Total assets | 1,158,696 | 1,743,614 | 115,059 | 430,888 | (1,752,704 | ) | 1,695,553 | |||||||||||||||||

| Amounts due to group companies | 88,887 | 253,725 | 71,038 | 230,319 | (643,969 | ) | — | |||||||||||||||||

| Accrued and other liabilities | 121,330 | 308,763 | 31,024 | 81,770 | — | 542,887 | ||||||||||||||||||

| Deferred revenue and customer advances | — | 53,501 | 12,971 | 4,001 | — | 70,473 | ||||||||||||||||||

| Total liabilities | 210,217 | 615,989 | 115,033 | 316,090 | (643,969 | ) | 613,360 | |||||||||||||||||

| Mezzanine equity | — | 9,655 | — | — | — | 9,655 | ||||||||||||||||||

| Total shareholders’ equity | 948,479 | 994,066 | (129 | ) | 114,798 | (1,108,735 | ) | 948,479 | ||||||||||||||||

| Noncontrolling interests | — | 123,904 | 155 | — | — | 124,059 | ||||||||||||||||||

| Total liabilities, mezzanine equity and equity | 1,158,696 | 1,743,614 | 115,059 | 430,888 | (1,752,704 | ) | 1,695,553 | |||||||||||||||||

Key Information Related to Doing Business in the People’s Republic of China

Risks and Uncertainties Related to Doing Business in the People’s Republic of China

We face various legal and operational risks and uncertainties as a company based in and primarily operating in China. Most of our operations are conducted in the PRC, and are governed by PRC laws, rules and regulations. Our PRC subsidiaries are subject to laws, rules and regulations applicable to foreign investment in China. Because PRC laws, rules and regulations are relatively new and quickly evolving, and because of the limited number of published decisions and the non-precedential nature of these decisions, and because the laws, rules and regulations often give the relevant regulator certain discretion in how to enforce them, the interpretation and enforcement of these laws, rules and regulations involve uncertainties and can be inconsistent and unpredictable. Therefore, it is possible that our existing operations may be found not to be in full compliance with relevant laws and regulations in the future. In addition, the PRC legal system is based in part on government policies and internal rules, some of which are not published on a timely basis or at all, and which may have a retroactive effect. As a result, we may not be aware of our violation of these policies and rules until after the occurrence of the violation. See “— D. Risk Factors — Risks Related to Doing Business in the People’s Republic of China — There are uncertainties regarding the

9

Table of Contents

interpretation and enforcement of PRC laws, rules and regulations, and changes in policies, laws, rules and regulations in the PRC could adversely affect us.”

The PRC government has significant oversight and discretion over the conduct of our business, and may intervene in or influence our operations through adopting and enforcing rules and regulatory requirements. For example, in recent years the PRC government, has enhanced regulation in areas such as anti-monopoly, anti-unfair competition, cybersecurity and data privacy. See “— D. Risk Factors — Risks Related to Our Business and Industry — We are subject to a broad range of laws and regulations, and future laws and regulations may impose additional requirements and other obligations that could materially and adversely affect our business, financial condition and results of operations, as well as the trading prices of our ADSs, Shares and/or other securities”; “— Claims or regulatory actions under competition laws against us may result in our being subject to fines, constraints on our business and damage to our reputation”; “— PRC regulations regarding acquisitions impose significant regulatory approval and review requirements, which could make it more difficult for us to pursue growth through acquisitions and subject us to fines or other administrative penalties”; and “— Our business is subject to complex and evolving domestic and international laws and regulations regarding privacy and data protection, which are subject to change and uncertain interpretation. Complying with these laws and regulations increases our cost of operations and may require changes to our data and other business practices or negatively affect our user growth and engagement. Failure to comply with these laws and regulations could result in claims, regulatory investigations, litigation or penalties, or otherwise negatively affect our business.” The Chinese government may further promulgate relevant laws, rules and regulations that may impose additional and significant obligations and liabilities on Chinese companies. These laws and regulations can be complex and stringent, and many are subject to change and uncertain interpretation, which could result in claims, change to our data and other business practices, regulatory investigations, penalties, increased cost of operations, or declines in user growth or engagement, or otherwise affect our business. As a result, the trading prices of our ADSs and Shares could significantly decline or become worthless.

In addition, the PRC government has enhanced its regulatory oversight of Chinese companies listing overseas, including enhanced oversight of overseas equity financing and listing by Chinese companies. Such new regulatory requirements could significantly limit or completely hinder our ability and the ability of our subsidiaries to obtain external financing through the issuance of equity securities overseas and cause the value of our securities, including our ADSs and Shares, to significantly decline or become worthless. See “— D. Risk Factors — Risks Related to Doing Business in the People’s Republic of China — There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations, and changes in policies, laws, rules and regulations in the PRC could adversely affect us”; and “— Risks Related to Our Business and Industry — We may need additional capital but may not be able to obtain it on favorable terms or at all.”

Permissions and Approvals Required to be Obtained from PRC Authorities for our Business Operations

In the opinion of Fangda Partners, our PRC legal counsel, our consolidated subsidiaries and the VIEs in China have obtained all major licenses, permissions and approvals from the competent PRC authorities that are necessary to the operations of our China commerce and cloud businesses, which accounted for a significant majority of our revenue in fiscal year 2023. In addition, we have implemented policies and control procedures to obtain and maintain the necessary licenses, permission and approvals to conduct our businesses. On the basis of the legal opinion issued by our PRC legal counsel and our internal policies and procedures, we believe that our consolidated subsidiaries and the VIEs in China have received the requisite licenses, permissions and approvals from the PRC authorities as are necessary for our business operations in China. Such licenses, permits, registrations and filings include, among others, Value-added Telecommunication License, License for Online Transmission of Audio-Visual Programs, Network Cultural Business License, Online Publishing Service License and License for Surveying and Mapping.

If we, our consolidated subsidiaries or the VIEs in China (i) do not maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, or (iii) applicable laws, regulations, or interpretations change, and we or the VIEs are required to obtain such permissions or approvals in the future, we may be unable to obtain such necessary approvals, permits, registrations or filings in a timely manner, or at all, and such approvals, permits, registrations or filings may be rescinded even if obtained. Any such circumstance may subject us to fines and other regulatory, civil or criminal liabilities, and we may be ordered by the competent PRC authorities to suspend relevant operations, which could materially and adversely affect our business, financial condition, results of operations and prospects. Please see “— D. Risk Factors — Risks Related to Our Business and Industry — We are subject to a broad range of laws and regulations, and future laws and regulations may impose additional requirements and other obligations that could materially and adversely affect our business, financial condition and results of operations, as well as the trading prices of our ADSs, Shares and/or other securities.”

10

Table of Contents